Page 296 - TSMC 2019 Annual Report

P. 296

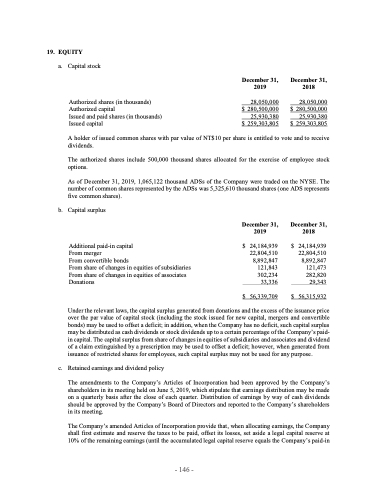

19. EQUITY

a. Capital stock

Authorized shares (in thousands) Authorized capital

Issued and paid shares (in thousands) Issued capital

December 31, 2019

28,050,000 $ 280,500,000 25,930,380 $ 259,303,805

December 31, 2018

28,050,000 $ 280,500,000 25,930,380 $ 259,303,805

A holder of issued common shares with par value of NT$10 per share is entitled to vote and to receive dividends.

The authorized shares include 500,000 thousand shares allocated for the exercise of employee stock options.

As of December 31, 2019, 1,065,122 thousand ADSs of the Company were traded on the NYSE. The number of common shares represented by the ADSs was 5,325,610 thousand shares (one ADS represents five common shares).

b. Capital surplus

Additional paid-in capital

From merger

From convertible bonds

From share of changes in equities of subsidiaries From share of changes in equities of associates Donations

December 31, 2019

December 31, 2018

$

24,184,939 22,804,510 8,892,847 121,843 302,234 33,336

$

24,184,939 22,804,510 8,892,847 121,473 282,820 29,343

$ 56,339,709

$ 56,315,932

Under the relevant laws, the capital surplus generated from donations and the excess of the issuance price over the par value of capital stock (including the stock issued for new capital, mergers and convertible bonds) may be used to offset a deficit; in addition, when the Company has no deficit, such capital surplus may be distributed as cash dividends or stock dividends up to a certain percentage of the Company’s paid- in capital. The capital surplus from share of changes in equities of subsidiaries and associates and dividend of a claim extinguished by a prescription may be used to offset a deficit; however, when generated from issuance of restricted shares for employees, such capital surplus may not be used for any purpose.

c. Retained earnings and dividend policy

The amendments to the Company’s Articles of Incorporation had been approved by the Company’s shareholders in its meeting held on June 5, 2019, which stipulate that earnings distribution may be made on a quarterly basis after the close of each quarter. Distribution of earnings by way of cash dividends should be approved by the Company’s Board of Directors and reported to the Company’s shareholders in its meeting.

The Company’s amended Articles of Incorporation provide that, when allocating earnings, the Company shall first estimate and reserve the taxes to be paid, offset its losses, set aside a legal capital reserve at 10% of the remaining earnings (until the accumulated legal capital reserve equals the Company’s paid-in

- 146 -