Page 295 - TSMC 2019 Annual Report

P. 295

Through the defined benefit plans under the R.O.C. Labor Standards Law, the Company is exposed to the following risks:

1) Investment risk: The pension funds are invested in equity and debt securities, bank deposits, etc. The investment is conducted at the discretion of the government’s designated authorities or under the mandated management. However, under the R.O.C. Labor Standards Law, the rate of return on assets shall not be less than the average interest rate on a two-year time deposit published by the local banks and the government is responsible for any shortfall in the event that the rate of return is less than the required rate of return.

2) Interest risk: A decrease in the government bond interest rate will increase the present value of the defined benefit obligation; however, this will be partially offset by an increase in the return on the debt investments of the plan assets.

Assuming a hypothetical decrease in interest rate at the end of the reporting period contributed to a decrease of 0.5% in the discount rate and all other assumptions were held constant, the present value of the defined benefit obligation would increase by NT$724,963 thousand and NT$921,750 thousand as of December 31, 2019 and 2018, respectively.

3) Salary risk: The present value of the defined benefit obligation is calculated by reference to the future salaries of plan participants. As such, an increase in the salary of the plan participants will increase the present value of the defined benefit obligation.

Assuming the expected salary rate increases by 0.5% at the end of the reporting period and all other assumptions were held constant, the present value of the defined benefit obligation would increase by NT$706,502 thousand and NT$901,629 thousand as of December 31, 2019 and 2018, respectively.

The sensitivity analysis presented above may not be representative of the actual change in the defined benefit obligation as it is unlikely that the change in assumptions would occur in isolation of one another as some of the assumptions may be correlated.

Furthermore, in presenting the above sensitivity analysis, the present value of the defined benefit obligation has been calculated using the projected unit credit method at the end of the reporting period, which is the same as that applied in calculating the defined benefit obligation liability.

The Company expects to make contributions of NT$230,864 thousand to the defined benefit plans in the next year starting from December 31, 2019. The weighted average duration of the defined benefit obligation is 10 years.

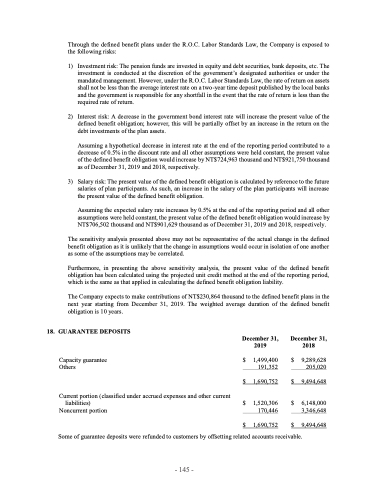

18. GUARANTEE DEPOSITS

December 31, 2019

December 31, 2018

$ 9,289,628 205,020

$ 9,494,648

$ 6,148,000 3,346,648

Capacity guarantee $ 1,499,400 Others 191,352

$ 1,690,752

Current portion (classified under accrued expenses and other current

liabilities) $ 1,520,306 Noncurrent portion 170,446

$ 1,690,752

Some of guarantee deposits were refunded to customers by offsetting related accounts receivable.

$ 9,494,648

- 145 -