Page 294 - TSMC 2019 Annual Report

P. 294

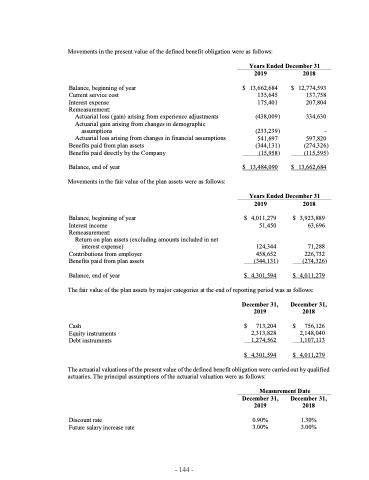

Movements in the present value of the defined benefit obligation were as follows:

Years Ended December 31

Balance, beginning of year Current service cost Interest expense Remeasurement:

Actuarial loss (gain) arising from experience adjustments Actuarial gain arising from changes in demographic

assumptions

Actuarial loss arising from changes in financial assumptions

Benefits paid from plan assets Benefits paid directly by the Company

Balance, end of year

Movements in the fair value of the plan assets were as follows:

Balance, beginning of year Interest income Remeasurement:

Return on plan assets (excluding amounts included in net interest expense)

Contributions from employer Benefits paid from plan assets

$

2019

13,662,684 135,645 175,401

(438,009)

(233,239) 541,697 (344,131)

(15,958) 13,484,090

$

2018

12,774,593 137,758 207,804

334,630

-

597,820 (274,326) (115,595)

13,662,684

$

$

$

Years Ended December 31

2019

4,011,279 51,450

124,344

458,652 (344,131)

2018

3,923,889 63,696

71,288 226,732

(274,326) 4,011,279

December 31, December 31,

$

Balance, end of year

The fair value of the plan assets by major categories at the end of reporting period was as follows:

$

4,301,594

$

Cash

Equity instruments Debt instruments

2019

$ 713,204 $ 2,313,828

2018

756,126 2,148,040 1,107,113

4,011,279

1,274,562 $ 4,301,594

$

The actuarial valuations of the present value of the defined benefit obligation were carried out by qualified actuaries. The principal assumptions of the actuarial valuation were as follows:

Discount rate

Future salary increase rate

December 31, 2019

0.90% 3.00%

December 31, 2018

1.30% 3.00%

- 144 -

Measurement Date