Page 183 - TSMC 2019 Annual Report

P. 183

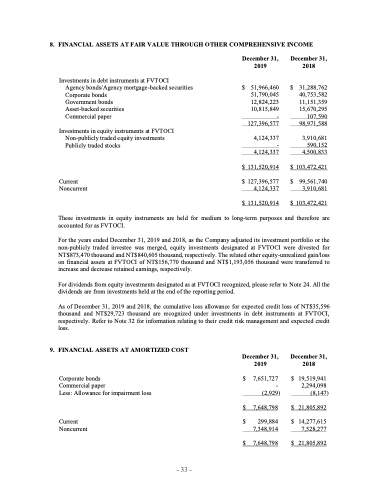

8. FINANCIAL ASSETS AT FAIR VALUE THROUGH OTHER COMPREHENSIVE INCOME

Investments in debt instruments at FVTOCI

Agency bonds/Agency mortgage-backed securities Corporate bonds

Government bonds

Asset-backed securities

Commercial paper

Investments in equity instruments at FVTOCI Non-publicly traded equity investments Publicly traded stocks

Current Noncurrent

$

31,288,762 40,753,582 11,151,359 15,670,295

107,590 98,971,588

3,910,681 590,152 4,500,833

December 31, 2019

$ 51,966,460 51,790,045 12,824,223 10,815,849 - 127,396,577

4,124,337 - 4,124,337

$ 131,520,914

$ 127,396,577 4,124,337

$ 131,520,914

December 31, 2018

$ 103,472,421

$ 99,561,740 3,910,681

$ 103,472,421

These investments in equity instruments are held for medium to long-term purposes and therefore are accounted for as FVTOCI.

For the years ended December 31, 2019 and 2018, as the Company adjusted its investment portfolio or the non-publicly traded investee was merged, equity investments designated at FVTOCI were divested for NT$873,470 thousand and NT$840,605 thousand, respectively. The related other equity-unrealized gain/loss on financial assets at FVTOCI of NT$156,770 thousand and NT$1,193,056 thousand were transferred to increase and decrease retained earnings, respectively.

For dividends from equity investments designated as at FVTOCI recognized, please refer to Note 24. All the dividends are from investments held at the end of the reporting period.

As of December 31, 2019 and 2018, the cumulative loss allowance for expected credit loss of NT$35,596 thousand and NT$29,723 thousand are recognized under investments in debt instruments at FVTOCI, respectively. Refer to Note 32 for information relating to their credit risk management and expected credit loss.

9. FINANCIAL ASSETS AT AMORTIZED COST

Corporate bonds

Commercial paper

Less: Allowance for impairment loss

Current Noncurrent

December 31, 2019

December 31, 2018

$

7,651,727 -

$

19,519,941 2,294,098

(2,929) $ 7,648,798

$ 299,884 7,348,914

$ 7,648,798

(8,147) $ 21,805,892

$ 14,277,615 7,528,277

$ 21,805,892

- 33 -