Page 184 - TSMC 2019 Annual Report

P. 184

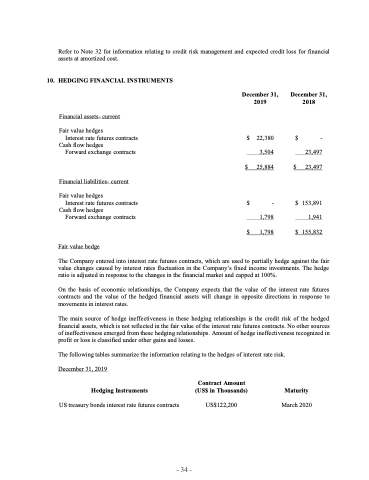

Refer to Note 32 for information relating to credit risk management and expected credit loss for financial assets at amortized cost.

10. HEDGINGFINANCIALINSTRUMENTS

Financial assets- current

Fair value hedges

Interest rate futures contracts

Cash flow hedges

Forward exchange contracts

Financial liabilities- current

Fair value hedges Interestratefuturescontracts

Cash flow hedges

Forward exchange contracts

Fair value hedge

December 31, 2019

$ 22,380 3,504 $ 25,884

$ - 1,798 $ 1,798

December 31, 2018

$ $

-

23,497 23,497

$ 153,891 1,941 $ 155,832

The Company entered into interest rate futures contracts, which are used to partially hedge against the fair

value changes caused by interest rates fluctuation in the Company’s fixed income investments. The hedge

ratio is adjusted in response to the changes in the financial market and capped at 100%.

On the basis of economic relationships, the Company expects that the value of the interest rate futures contracts and the value of the hedged financial assets will change in opposite directions in response to movements in interest rates.

The main source of hedge ineffectiveness in these hedging relationships is the credit risk of the hedged financial assets, which is not reflected in the fair value of the interest rate futures contracts. No other sources of ineffectiveness emerged from these hedging relationships. Amount of hedge ineffectiveness recognized in profit or loss is classified under other gains and losses.

The following tables summarize the information relating to the hedges of interest rate risk. December 31, 2019

Contract Amount

Hedging Instruments (US$ in Thousands) Maturity

US treasury bonds interest rate futures contracts US$122,200 March 2020

- 34 -