Page 181 - TSMC 2019 Annual Report

P. 181

from the commencement date until the exercise date of the option. Main factors considered include contractual terms and conditions covered by the optional periods, and the importance of the underlying asset to the lessee’s operations, etc. The lease term is reassessed if a significant change in circumstances that are within the control of the Company occurs.

Key Sources of Estimation and Uncertainty

Estimation of Sales Returns and Allowances

Sales returns and other allowance is estimated and recorded based on historical experience and in consideration of different contractual terms. The amount is deducted from revenue in the same period the related revenue is recorded. The Company periodically reviews the reasonableness of the estimates.

Valuation of Inventory

Inventories are stated at the lower of cost or net realizable value, and the Company uses estimate to determine the net realizable value of inventory at the end of each reporting period.

The Company estimates the net realizable value of inventory for normal waste, obsolescence and unmarketable items at the end of reporting period and then writes down the cost of inventories to net realizable value. The net realizable value of the inventory is determined mainly based on assumptions of future demand within a specific time horizon.

Impairment of Tangible Assets, Right-of-use Assets and Intangible Assets Other than Goodwill

In the process of evaluating the potential impairment of tangible assets, right-of-use assets and intangible assets other than goodwill, the Company determines the independent cash flows, useful lives, expected future revenue and expenses related to the specific asset groups with the consideration of the nature of semiconductor industry. Any change in these estimates based on changed economic conditions or business strategies could result in significant impairment charges or reversal in future years.

Realization of Deferred Income Tax Assets

Deferred tax assets are recognized to the extent that it is probable that future taxable profits will be available against which those deferred tax assets can be utilized. Assessment of the realization of the deferred tax assets requires subjective judgment and estimate, including the future revenue growth and profitability, tax holidays, the amount of tax credits can be utilized and feasible tax planning strategies. Any changes in the global economic environment, the industry trends and relevant laws and regulations could result in significant adjustments to the deferred tax assets.

Determination of Lessees’ Incremental Borrowing Rates

In determining a lessee’s incremental borrowing rate used in discounting lease payments, the Company mainly takes into account the market risk-free rates, the estimated lessee’s credit spreads and secured status in a similar economic environment.

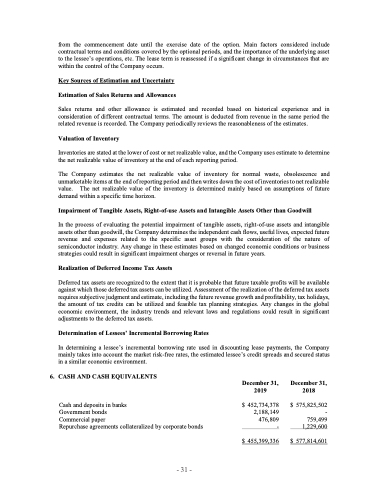

6. CASH AND CASH EQUIVALENTS

Cash and deposits in banks

Government bonds

Commercial paper

Repurchase agreements collateralized by corporate bonds

December 31, 2019

$ 452,734,378 2,188,149 476,809 -

December 31, 2018

$ 575,825,502 - 759,499 1,229,600

$ 577,814,601

$ 455,399,336

- 31 -