Page 167 - TSMC 2018 Annual Report

P. 167

(5) With the retrospective adoption of IFRS 9 by associates accounted for using equity method, the corresponding adjustments made by the Company would result in an increase in investments accounted for using equity method of NT$8,259 thousand, a decrease in other equity- unrealized gain or loss on financial assets at FVTOCI of NT$23,616 thousand, a decrease in other equity- unrealized gain or loss on available-for-sale financial assets of NT$2,110 thousand and an increase in retained earnings of NT$33,985 thousand on January 1, 2018.

Hedge accounting

The Company prospectively applies the requirements for hedge accounting upon initial application of IFRS 9. In addition, due to the amendments to the Regulations Governing the Preparation of Financial Reports by Securities Issuers, all derivative and non-derivative financial assets and financial liabilities which are designated as hedging instruments are presented as financial assets and financial liabilities for hedging starting 2018.

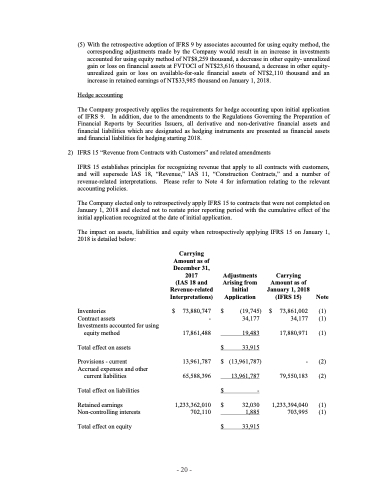

2) IFRS 15 “Revenue from Contracts with Customers” and related amendments

IFRS 15 establishes principles for recognizing revenue that apply to all contracts with customers,

and will supersede IAS 18, “Revenue,” IAS 11, “Construction Contracts,” and a number of

revenue-related interpretations. Please refer to Note 4 for information relating to the relevant accounting policies.

The Company elected only to retrospectively apply IFRS 15 to contracts that were not completed on January 1, 2018 and elected not to restate prior reporting period with the cumulative effect of the initial application recognized at the date of initial application.

The impact on assets, liabilities and equity when retrospectively applying IFRS 15 on January 1, 2018 is detailed below:

Inventories

Contract assets

Investments accounted for using

$ (19,745) $ 73,861,002 (1) 34,177 34,177 (1)

19,483 17,880,971 (1)

equity method 17,861,488 Total effect on assets

$

$ (13,961,787) - (2)

13,961,787 79,550,183 (2) $ -

$ 32,030 1,233,394,040 (1) 1,885 703,995 (1)

$ 33,915

Carrying Amount as of December 31, 2017

(IAS 18 and Revenue-related Interpretations)

$ 73,880,747 -

Adjustments Arising from Initial Application

Carrying Amount as of January 1, 2018

(IFRS 15) Note

33,915

Provisions - current Accrued expenses and other

current liabilities Total effect on liabilities

Retained earnings Non-controlling interests

Total effect on equity

13,961,787 65,588,396

1,233,362,010 702,110

- 20 -