Page 169 - TSMC 2018 Annual Report

P. 169

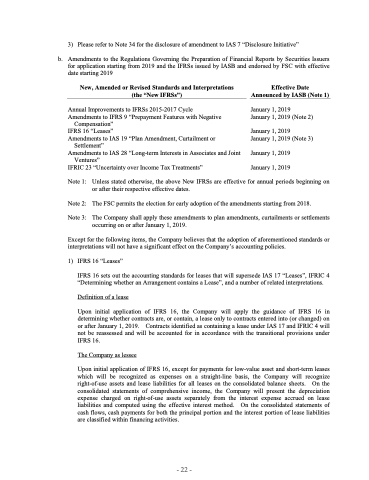

3) Please refer to Note 34 for the disclosure of amendment to IAS 7 “Disclosure Initiative”

b. Amendments to the Regulations Governing the Preparation of Financial Reports by Securities Issuers for application starting from 2019 and the IFRSs issued by IASB and endorsed by FSC with effective date starting 2019

New, Amended or Revised Standards and Interpretations

(the “New IFRSs”)

Annual Improvements to IFRSs 2015-2017 Cycle

Amendments to IFRS 9 “Prepayment Features with Negative Compensation”

IFRS 16 “Leases”

Amendments to IAS 19 “Plan Amendment, Curtailment or

Settlement”

Amendments to IAS 28 “Long-term Interests in Associates and Joint

Ventures”

IFRIC 23 “Uncertainty over Income Tax Treatments”

Effective Date Announced by IASB (Note 1)

January 1, 2019

January 1, 2019 (Note 2)

January 1, 2019

January 1, 2019 (Note 3)

January 1, 2019

January 1, 2019

Note 1:

Note 2: Note 3:

Unless stated otherwise, the above New IFRSs are effective for annual periods beginning on or after their respective effective dates.

The FSC permits the election for early adoption of the amendments starting from 2018.

The Company shall apply these amendments to plan amendments, curtailments or settlements occurring on or after January 1, 2019.

Except for the following items, the Company believes that the adoption of aforementioned standards or interpretations will not have a significant effect on the Company’s accounting policies.

1) IFRS 16 “Leases”

IFRS 16 sets out the accounting standards for leases that will supersede IAS 17 “Leases”, IFRIC 4

“Determining whether an Arrangement contains a Lease”, and a number of related interpretations.

Definition of a lease

Upon initial application of IFRS 16, the Company will apply the guidance of IFRS 16 in determining whether contracts are, or contain, a lease only to contracts entered into (or changed) on or after January 1, 2019. Contracts identified as containing a lease under IAS 17 and IFRIC 4 will not be reassessed and will be accounted for in accordance with the transitional provisions under IFRS 16.

The Company as lessee

Upon initial application of IFRS 16, except for payments for low-value asset and short-term leases which will be recognized as expenses on a straight-line basis, the Company will recognize right-of-use assets and lease liabilities for all leases on the consolidated balance sheets. On the consolidated statements of comprehensive income, the Company will present the depreciation expense charged on right-of-use assets separately from the interest expense accrued on lease liabilities and computed using the effective interest method. On the consolidated statements of cash flows, cash payments for both the principal portion and the interest portion of lease liabilities are classified within financing activities.

- 22 -