Page 314 - TSMC 2019 Annual Report

P. 314

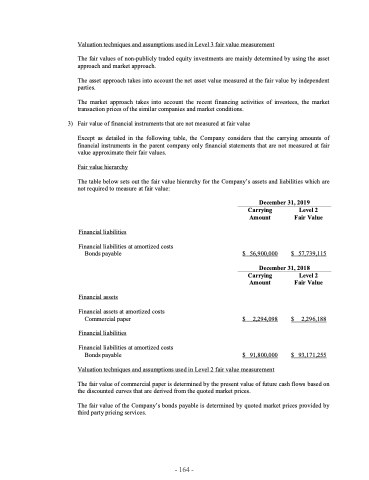

Valuation techniques and assumptions used in Level 3 fair value measurement

The fair values of non-publicly traded equity investments are mainly determined by using the asset approach and market approach.

The asset approach takes into account the net asset value measured at the fair value by independent parties.

The market approach takes into account the recent financing activities of investees, the market transaction prices of the similar companies and market conditions.

3) Fair value of financial instruments that are not measured at fair value

Except as detailed in the following table, the Company considers that the carrying amounts of financial instruments in the parent company only financial statements that are not measured at fair value approximate their fair values.

Fair value hierarchy

The table below sets out the fair value hierarchy for the Company’s assets and liabilities which are not required to measure at fair value:

Financial liabilities

Financial liabilities at amortized costs Bonds payable

Financial assets

Financial assets at amortized costs Commercial paper

Financial liabilities

Financial liabilities at amortized costs Bonds payable

The fair value of commercial paper is determined by the present value of future cash flows based on the discounted curves that are derived from the quoted market prices.

The fair value of the Company’s bonds payable is determined by quoted market prices provided by third party pricing services.

December 31, 2019

Carrying Amount

$ 56,900,000

Level 2 Fair Value

$ 57,739,115

December 31, 2018

Carrying Amount

$ 2,294,098

Level 2 Fair Value

$ 2,296,188

$ 93,171,255

$ 91,800,000 Valuation techniques and assumptions used in Level 2 fair value measurement

- 164 -