Page 299 - TSMC 2018 Annual Report

P. 299

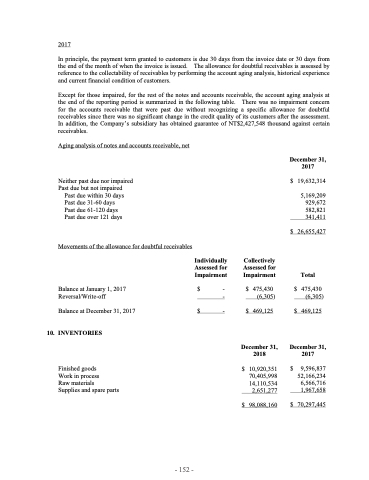

2017

In principle, the payment term granted to customers is due 30 days from the invoice date or 30 days from the end of the month of when the invoice is issued. The allowance for doubtful receivables is assessed by reference to the collectability of receivables by performing the account aging analysis, historical experience and current financial condition of customers.

Except for those impaired, for the rest of the notes and accounts receivable, the account aging analysis at the end of the reporting period is summarized in the following table. There was no impairment concern for the accounts receivable that were past due without recognizing a specific allowance for doubtful receivables since there was no significant change in the credit quality of its customers after the assessment. In addition, the Company’s subsidiary has obtained guarantee of NT$2,427,548 thousand against certain receivables.

Aging analysis of notes and accounts receivable, net

Neither past due nor impaired Past due but not impaired

Past due within 30 days Past due 31-60 days Past due 61-120 days Past due over 121 days

Movements of the allowance for doubtful receivables

Balance at January 1, 2017 Reversal/Write-off

Balance at December 31, 2017

10. INVENTORIES

Finished goods

Work in process

Raw materials

Supplies and spare parts

December 31, 2017

$

19,632,314

5,169,209 929,672 582,821 341,411

Individually Assessed for Impairment

Collectively Assessed for Impairment

$ 475,430 (6,305)

$ 469,125

December 31, 2018

$ 10,920,351 70,405,998 14,110,534 2,651,277

$ 98,088,160

$ 26,655,427

Total

$ 475,430 (6,305)

$ 469,125

December 31, 2017

$

$ -

- -

$

9,596,837 52,166,234 6,566,716 1,967,658

$ 70,297,445

- 152 -