Page 298 - TSMC 2018 Annual Report

P. 298

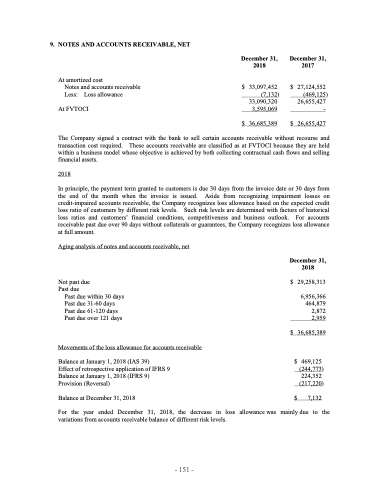

9. NOTES AND ACCOUNTS RECEIVABLE, NET

At amortized cost

Notes and accounts receivable Less: Loss allowance

At FVTOCI

$

33,097,452 (7,132)

33,090,320 3,595,069

$

$

27,124,552 (469,125)

26,655,427 -

26,655,427

December 31, 2018

December 31, 2017

$ 36,685,389

The Company signed a contract with the bank to sell certain accounts receivable without recourse and transaction cost required. These accounts receivable are classified as at FVTOCI because they are held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

2018

In principle, the payment term granted to customers is due 30 days from the invoice date or 30 days from the end of the month when the invoice is issued. Aside from recognizing impairment losses on credit-impaired accounts receivable, the Company recognizes loss allowance based on the expected credit loss ratio of customers by different risk levels. Such risk levels are determined with factors of historical loss ratios and customers’ financial conditions, competitiveness and business outlook. For accounts receivable past due over 90 days without collaterals or guarantees, the Company recognizes loss allowance at full amount.

Aging analysis of notes and accounts receivable, net

Not past due Past due

Past due within 30 days Past due 31-60 days Past due 61-120 days Past due over 121 days

Movements of the loss allowance for accounts receivable

Balance at January 1, 2018 (IAS 39)

Effect of retrospective application of IFRS 9 Balance at January 1, 2018 (IFRS 9) Provision (Reversal)

Balance at December 31, 2018

December 31, 2018

$

29,258,313

6,956,366 464,879 2,872 2,959

$ 36,685,389

$

$

469,125 (244,773) 224,352 (217,220)

7,132

For the year ended December 31, 2018, the decrease in loss allowancewas mainlydue to the variations from accounts receivable balance of different risk levels.

- 151 -