Page 277 - TSMC 2018 Annual Report

P. 277

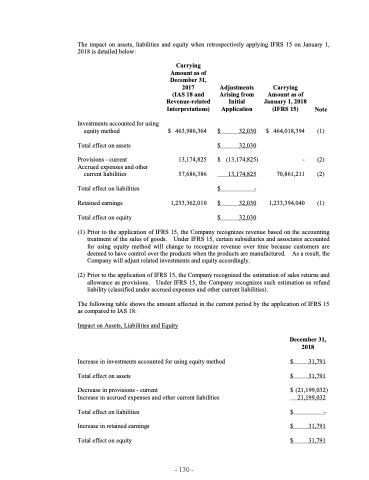

The impact on assets, liabilities and equity when retrospectively applying IFRS 15 on January 1, 2018 is detailed below:

Investments accounted for using equity method

Total effect on assets

Provisions - current Accrued expenses and other

current liabilities Total effect on liabilities Retained earnings

Total effect on equity

$

463,986,364 $ 32,030 $ 32,030

$

(IFRS 15) Note

464,018,394 (1)

- (2) 70,861,211 (2)

Carrying Amount as of December 31,

2017 Adjustments (IAS 18 and Arising from

Revenue-related Initial Interpretations) Application

Carrying Amount as of January 1, 2018

13,174,825 $ (13,174,825) 57,686,386 13,174,825 $ - 1,233,362,010 $ 32,030 $ 32,030

1,233,394,040 (1)

(1) Prior to the application of IFRS 15, the Company recognizes revenue based on the accounting treatment of the sales of goods. Under IFRS 15, certain subsidiaries and associates accounted for using equity method will change to recognize revenue over time because customers are deemed to have control over the products when the products are manufactured. As a result, the Company will adjust related investments and equity accordingly.

(2) Prior to the application of IFRS 15, the Company recognized the estimation of sales returns and allowance as provisions. Under IFRS 15, the Company recognizes such estimation as refund liability (classified under accrued expenses and other current liabilities).

The following table shows the amount affected in the current period by the application of IFRS 15 as compared to IAS 18:

Impact on Assets, Liabilities and Equity

December 31, 2018

$ 31,791

$ 31,791

$ (21,199,032) 21,199,032

$-

$ 31,791

$ 31,791

Increase in investments accounted for using equity method

Total effect on assets

Decrease in provisions - current

Increase in accrued expenses and other current liabilities

Total effect on liabilities Increase in retained earnings Total effect on equity

- 130 -