Page 302 - TSMC 2019 Annual Report

P. 302

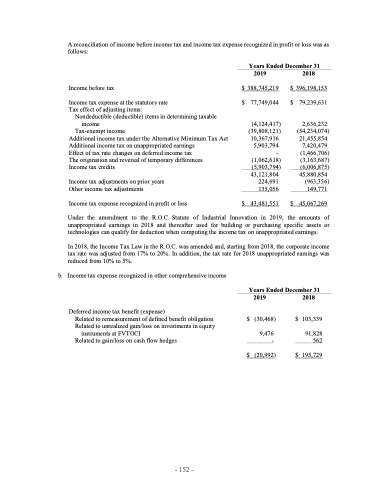

A reconciliation of income before income tax and income tax expense recognized in profit or loss was as follows:

Income before tax

Income tax expense at the statutory rate Tax effect of adjusting items:

Nondeductible (deductible) items in determining taxable income

Tax-exempt income

Additional income tax under the Alternative Minimum Tax Act Additional income tax on unappropriated earnings

Effect of tax rate changes on deferred income tax

The origination and reversal of temporary differences

Income tax credits

Income tax adjustments on prior years Other income tax adjustments

Income tax expense recognized in profit or loss

2019

$ 388,745,219

2018

$ 396,198,153

Years Ended December 31

$

77,749,044

(4,124,417) (39,808,121)

10,367,916 5,903,794 -

(1,062,618) (5,903,794)

43,121,804 224,691 135,056

43,481,551

$

79,239,631

2,636,232 (54,234,074)

21,455,854 7,420,479

(1,466,706) (3,163,687) (6,006,875)

45,880,854 (963,356)

149,771 45,067,269

$

$

Under the amendment to the R.O.C Statute of Industrial Innovation in 2019, the amounts of unappropriated earnings in 2018 and thereafter used for building or purchasing specific assets or technologies can qualify for deduction when computing the income tax on unappropriated earnings.

In 2018, the Income Tax Law in the R.O.C. was amended and, starting from 2018, the corporate income tax rate was adjusted from 17% to 20%. In addition, the tax rate for 2018 unappropriated earnings was reduced from 10% to 5%.

b. Income tax expense recognized in other comprehensive income

Deferred income tax benefit (expense)

Related to remeasurement of defined benefit obligation Related to unrealized gain/loss on investments in equity

instruments at FVTOCI

Related to gain/loss on cash flow hedges

Years Ended December 31

2019

$ (30,468)

9,476 -

$ (20,992)

2018

$ 103,339

91,828 562

$ 195,729

- 152 -