Page 187 - TSMC 2019 Annual Report

P. 187

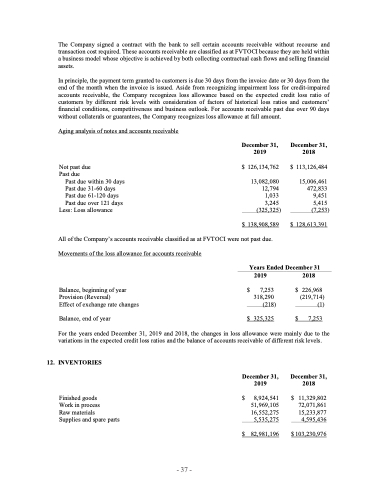

The Company signed a contract with the bank to sell certain accounts receivable without recourse and transaction cost required. These accounts receivable are classified as at FVTOCI because they are held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

In principle, the payment term granted to customers is due 30 days from the invoice date or 30 days from the end of the month when the invoice is issued. Aside from recognizing impairment loss for credit-impaired accounts receivable, the Company recognizes loss allowance based on the expected credit loss ratio of customers by different risk levels with consideration of factors of historical loss ratios and customers’ financial conditions, competitiveness and business outlook. For accounts receivable past due over 90 days without collaterals or guarantees, the Company recognizes loss allowance at full amount.

Aging analysis of notes and accounts receivable

Not past due Past due

Past due within 30 days Past due 31-60 days Past due 61-120 days Past due over 121 days

Less: Loss allowance

December 31, 2019

$ 126,134,762

13,082,080 12,794 1,033 3,245

(325,325) $ 138,908,589

December 31, 2018

$ 113,126,484

15,006,461 472,833 9,451 5,415

(7,253) $ 128,613,391

All of the Company’s accounts receivable classified as at FVTOCI were not past due. Movements of the loss allowance for accounts receivable

Years Ended December 31

Balance,beginningofyear Provision (Reversal)

Effect of exchange rate changes

Balance, end of year

$

2019

7,253 318,290

2018

$ 226,968 (219,714) (1)

$ 7,253

(218) $ 325,325

For the years ended December 31, 2019 and 2018, the changes in loss allowance were mainly due to the variations in the expected credit loss ratios and the balance of accounts receivable of different risk levels.

12. INVENTORIES

Finished goods

Work in process

Raw materials

Supplies and spare parts

December 31, 2019

December 31, 2018

$

$

8,924,541 51,969,105 16,552,275

5,535,275 82,981,196

$

11,329,802 72,071,861 15,233,877

4,595,436 $ 103,230,976

- 37 -