Page 167 - TSMC 2019 Annual Report

P. 167

The Company as lessee

Except for payments for short-term leases which are recognized as expenses on a straight-line basis, the Company recognizes right-of-use assets and lease liabilities for all leases on the consolidated balance sheets. On the consolidated statements of comprehensive income, the Company presents the depreciation expense charged on right-of-use assets separately from the interest expense accrued on lease liabilities, which is computed using the effective interest method. On the consolidated statements of cash flows, cash payments for both the principal portion and the interest portion of lease liabilities are classified within financing activities.

The Company applies IFRS 16 retrospectively with the cumulative effect of the initial application recognized at the date of initial application but does not restate comparative information.

Leases agreements classified as operating leases under IAS 17, except for short-term leases, are measured at the present value of the remaining lease payments, discounted using the lessee’s incremental borrowing rate on January 1, 2019. Right-of-use assets are measured at an amount equal to the lease liabilities, adjusted by the amount of any prepaid or accrued lease payments. Right-of-use assets are subject to impairment testing under IAS 36.

The Company applied the following practical expedients to measure right-of-use assets and lease liabilities on January 1, 2019:

a) The Company applied a single discount rate to a portfolio of leases with reasonably similar characteristics to measure lease liabilities.

b) The Company accounted for those leases for which the lease term ends on or before December 31, 2019 as short-term leases.

c) Except for lease payments, the Company excluded incremental costs of obtaining the lease from right-of-use assets on January 1, 2019.

d) The Company determined lease terms (e.g. lease periods) based on the projected status on January 1, 2019, to measure lease liabilities.

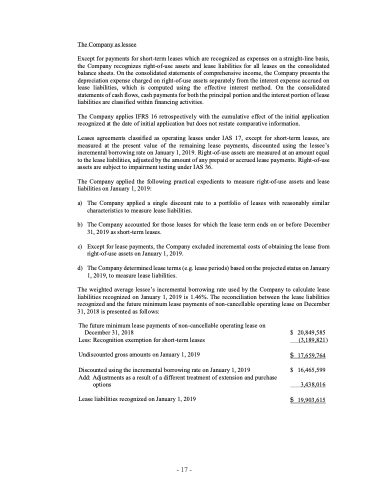

The weighted average lessee’s incremental borrowing rate used by the Company to calculate lease liabilities recognized on January 1, 2019 is 1.46%. The reconciliation between the lease liabilities recognized and the future minimum lease payments of non-cancellable operating lease on December 31, 2018 is presented as follows:

The future minimum lease payments of non-cancellable operating lease on December 31, 2018

Less: Recognition exemption for short-term leases Undiscounted gross amounts on January 1, 2019

Discounted using the incremental borrowing rate on January 1, 2019

Add: Adjustments as a result of a different treatment of extension and purchase

options

Lease liabilities recognized on January 1, 2019

$ 20,849,585 (3,189,821)

$ 17,659,764 $ 16,465,599 3,438,016

$ 19,903,615

- 17 -