Page 280 - TSMC 2018 Annual Report

P. 280

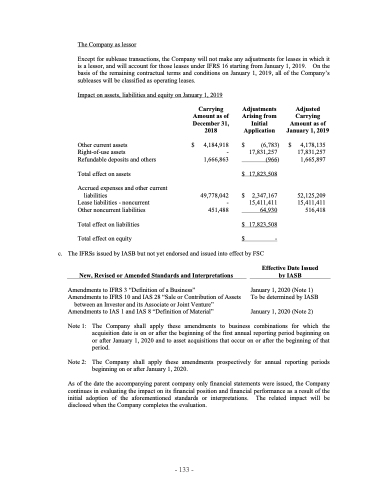

The Company as lessor

Except for sublease transactions, the Company will not make any adjustments for leases in which it is a lessor, and will account for those leases under IFRS 16 starting from January 1, 2019. On the basis of the remaining contractual terms and conditions on January 1, 2019, all of the Company’s subleases will be classified as operating leases.

Impact on assets, liabilities and equity on January 1, 2019

Other current assets Right-of-use assets

Refundable deposits and others

Total effect on assets

Accrued expenses and other current liabilities

Lease liabilities - noncurrent Other noncurrent liabilities

Total effect on liabilities

$

2018 Application

4,184,918 $ (6,783) - 17,831,257

1,666,863 (966) $ 17,823,508

49,778,042 $ 2,347,167 - 15,411,411 451,488 64,930

$ 17,823,508

$

4,178,135 17,831,257 1,665,897

52,125,209 15,411,411 516,418

Carrying Adjustments Amount as of Arising from December 31, Initial

Adjusted

Carrying Amount as of January 1, 2019

Total effect on equity

c. The IFRSs issued by IASB but not yet endorsed and issued into effect by FSC

New, Revised or Amended Standards and Interpretations

Amendments to IFRS 3 “Definition of a Business”

Amendments to IFRS 10 and IAS 28 “Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture” Amendments to IAS 1 and IAS 8 “Definition of Material”

Effective Date Issued by IASB

January 1, 2020 (Note 1) To be determined by IASB

January 1, 2020 (Note 2)

$

-

Note1:

Note 2:

The Company shall apply these amendments to business combinations for which the acquisition date is on or after the beginning of the first annual reporting period beginning on or after January 1, 2020 and to asset acquisitions that occur on or after the beginning of that period.

The Company shall apply these amendments prospectively for annual reporting periods beginning on or after January 1, 2020.

As of the date the accompanying parent company only financial statements were issued, the Company continues in evaluating the impact on its financial position and financial performance as a result of the initial adoption of the aforementioned standards or interpretations. The related impact will be disclosed when the Company completes the evaluation.

- 133 -