Page 192 - TSMC 2018 Annual Report

P. 192

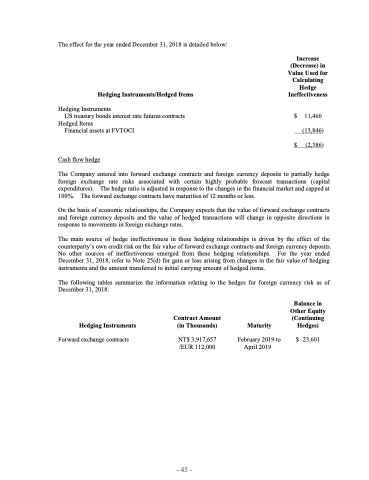

The effect for the year ended December 31, 2018 is detailed below:

Hedging Instruments/Hedged Items

Hedging Instruments

US treasury bonds interest rate futures contracts

Hedged Items

Financial assets at FVTOCI

Cash flow hedge

Increase (Decrease) in Value Used for Calculating Hedge Ineffectiveness

$

$

11,460 (13,846) (2,386)

The Company entered into forward exchange contracts and foreign currency deposits to partially hedge foreign exchange rate risks associated with certain highly probable forecast transactions (capital expenditures). The hedge ratio is adjusted in response to the changes in the financial market and capped at 100%. The forward exchange contracts have maturities of 12 months or less.

On the basis of economic relationships, the Company expects that the value of forward exchange contracts and foreign currency deposits and the value of hedged transactions will change in opposite directions in response to movements in foreign exchange rates.

The main source of hedge ineffectiveness in these hedging relationships is driven by the effect of the counterparty’s own credit risk on the fair value of forward exchange contracts and foreign currency deposits. No other sources of ineffectiveness emerged from these hedging relationships. For the year ended December 31, 2018, refer to Note 25(d) for gain or loss arising from changes in the fair value of hedging instruments and the amount transferred to initial carrying amount of hedged items.

The following tables summarize the information relating to the hedges for foreign currency risk as of December 31, 2018.

Hedging Instruments

Forward exchange contracts

Contract Amount (in Thousands)

NT$ 3,917,657 /EUR 112,000

Maturity

February 2019 to April 2019

Balance in Other Equity (Continuing Hedges)

$ 23,601

- 45 -