Page 187 - TSMC 2018 Annual Report

P. 187

conditions to ensure the appropriateness of fair value measurement of non-publicly traded equity investments.

Valuation of Inventory

Inventories are stated at the lower of cost or net realizable value, and the Company uses judgment and estimate to determine the net realizable value of inventory at the end of each reporting period.

The Company estimates the net realizable value of inventory for obsolescence and unmarketable items at the end of reporting period and then writes down the cost of inventories to net realizable value. The net realizable value of the inventory is mainly determined based on assumptions of future demand within a specific time horizon.

Recognition and Measurement of Defined Benefit Plans

Net defined benefit liability and the resulting defined benefit costs under defined benefit pension plans are calculated using the Projected Unit Credit Method. Actuarial assumptions comprise the discount rate, rate of employee turnover, and future salary increase rate. Changes in economic circumstances and market conditions will affect these assumptions and may have a material impact on the amount of the expense and the liability.

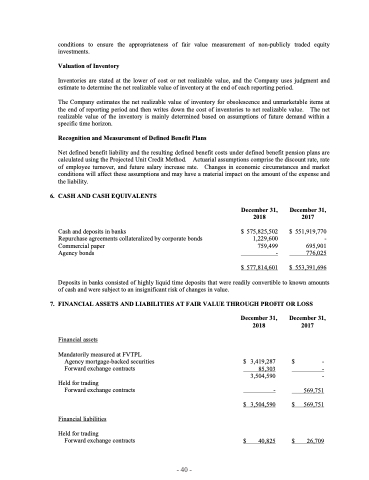

6. CASH AND CASH EQUIVALENTS

Cash and deposits in banks

Repurchase agreements collateralized by corporate bonds Commercial paper

Agency bonds

December 31, 2018

$ 575,825,502 1,229,600 759,499 -

$ 577,814,601

December 31, 2017

$ 551,919,770 - 695,901 776,025

$ 553,391,696

Deposits in banks consisted of highly liquid time deposits that were readily convertible to known amounts of cash and were subject to an insignificant risk of changes in value.

7. FINANCIAL ASSETS AND LIABILITIES AT FAIR VALUE THROUGH PROFIT OR LOSS

Financial assets

Mandatorily measured at FVTPL Agency mortgage-backed securities Forward exchange contracts

Held for trading

Forward exchange contracts

Financial liabilities

Held for trading

Forward exchange contracts

$

- - -

December 31, 2018

$ 3,419,287 85,303 3,504,590

- $ 3,504,590

$ 40,825

December 31, 2017

569,751 $ 569,751

$ 26,709

- 40 -