and Independent Auditors’ Report

- INDEPENDENT AUDITORS' REPORT

- PARENT COMPANY ONLY BALANCE SHEETS

- PARENT COMPANY ONLY STATEMENTS OF COMPREHENSIVE INCOME

- PARENT COMPANY ONLY STATEMENTS OF CHANGES IN EQUITY

- PARENT COMPANY ONLY STATEMENTS OF CASH FLOWS

- NOTES TO PARENT COMPANY ONLY FINANCIAL STATEMENTS

- THE CONTENTS OF STATEMENTS OF MAJOR ACCOUNTING ITEMS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

38. |

FIRST-TIME ADOPTION OF PARENT COMPANY ONLY FINANCIAL STATEMENTS ACCOUNTING STANDARDS |

|---|

The transition to Accounting Standards Used in Preparation of the Parent Company Only Financial Statements was on January 1, 2012 (the transition date). The effects on the Company’s parent company only balance sheets as of December 31, 2012 and January 1, 2012 as well as the parent company only statements of comprehensive income for the year ended December 31, 2012, were as follows:

a. |

Exemptions |

||||||

|---|---|---|---|---|---|---|---|

Except for optional exemptions and mandatory exceptions, the Company retrospectively applied Accounting Standards Used in Preparation of the Parent Company Only Financial Statements in its opening balance sheet at the date of transition, January 1, 2012. |

|||||||

|

b. |

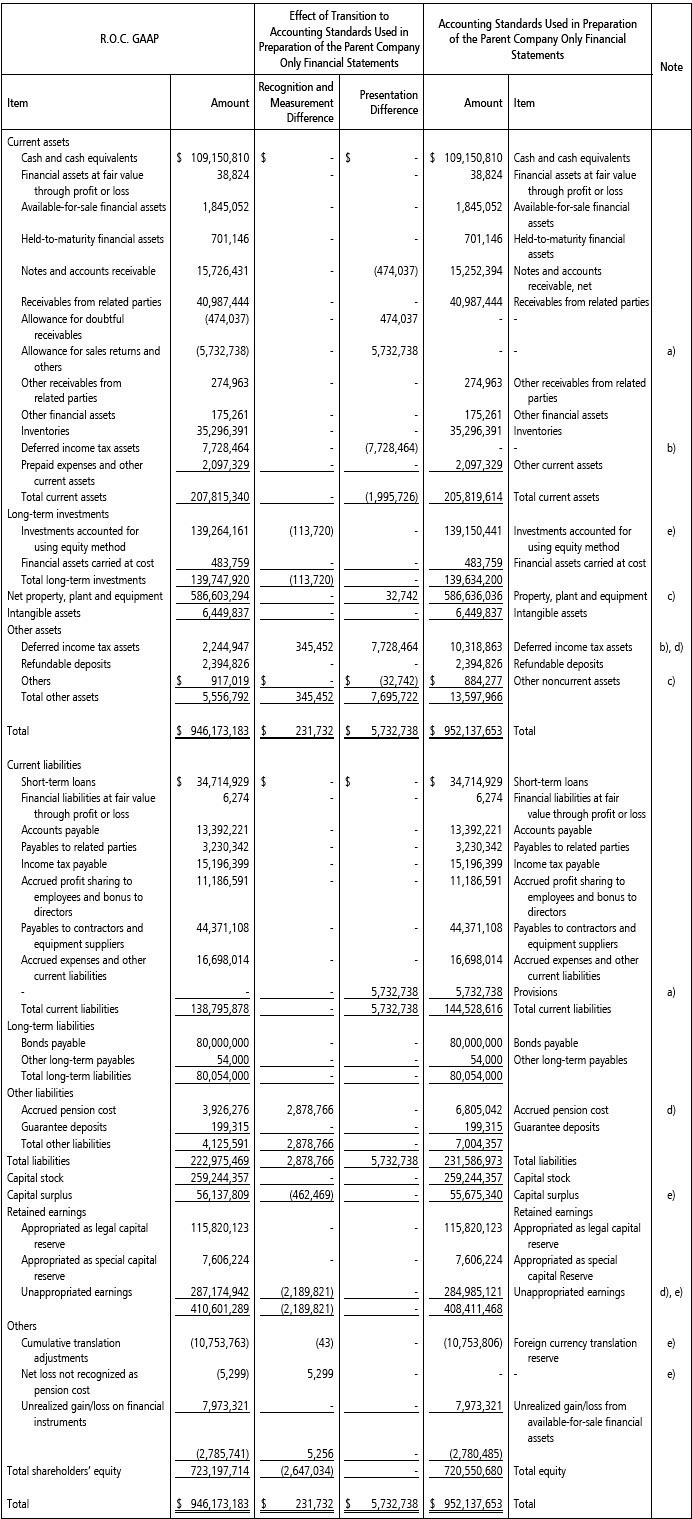

Reconciliation of parent company only balance sheet as of December 31, 2012 |

|---|

c. |

Reconciliation of parent company only balance sheet as of January 1, 2012 |

|---|

d. |

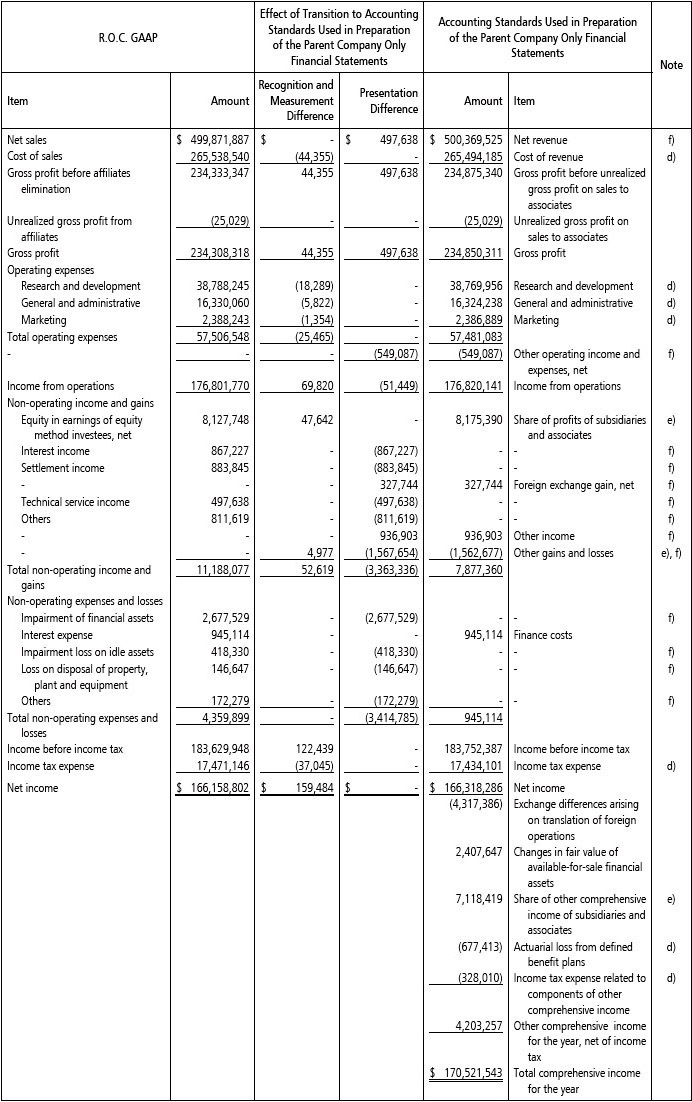

Reconciliation of parent company only statement of comprehensive income for the year ended December 31, 2012 |

|---|

e. |

Significant reconciliation differences in statement of cash flows for the year ended December 31, 2012 |

|---|---|

| For the year ended December 31, 2012, the Company partially disposed and acquired its interests in subsidiaries without the loss of control with the cash inflows and cash outflows of NT$587,902 thousand and NT$2,259,244 thousand, respectively. Under R.O.C. GAAP, such cash flows were classified as investing activities. However, under Accounting Standards Used in Preparation of the Parent Company Only Financial Statements, such cash flows were classified as financing activities. The Company prepared the statement of cash flows using the indirect method under R.O.C. GAAP, in which the interest received is not required to be disclosed separately; instead, the interest received and the interest paid are included within the operating activities in the statement of cash flows. However, according to Accounting Standards Used in Preparation of the Parent Company Only Financial Statements for the year ended December 31, 2012, the interest received of NT$834,314 thousand should be disclosed separately in the investing activities; and the interest paid of NT$670,165 thousand should be disclosed in the financing activities based on their nature, respectively. Except for the above differences, there are no other significant differences between R.O.C. GAAP and Accounting Standards Used in Preparation of the Parent Company Only Financial Statements in the parent company only statement of cash flows. |

f. |

Notes to the reconciliation of the significant differences: |

||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|