and Independent Auditors’ Report

- REPRESENTATION LETTER

- INDEPENDENT AUDITORS' REPORT

- CONSOLIDATED BALANCE SHEETS

- CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

- CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

- CONSOLIDATED STATEMENTS OF CASH FLOWS

- NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

43. |

FIRST-TIME ADOPTION OF TAIWAN-IFRSs |

|---|

a. |

Basis of preparation for financial information under Taiwan-IFRSs |

The Company prepares consolidated financial statements for the year ended December 31, 2013 under Taiwan-IFRSs. As the basis of the preparation, the Company not only follows the significant accounting policies stated in Note 4 but also applies IFRS 1. |

b. |

Exemptions from IFRS 1 |

IFRS 1 establishes the procedures for the Company’s first consolidated financial statements prepared in accordance with Taiwan-IFRSs. According to IFRS 1, the Company is required to determine the accounting policies under Taiwan-IFRSs and retrospectively apply those accounting policies in its opening balance sheet at the date of transition to Taiwan-IFRSs; except for optional exemptions and mandatory exceptions to such retrospective application provided under IFRS 1. The main optional exemptions the Company adopted are summarized as follows: |

|

| 1) Business combinations. The Company elected not to apply IFRS 3, “Business Combinations,” retrospectively to 2) Employee benefits. The Company elected to recognize all cumulative actuarial gains and losses in retained earnings as 3) Share-based payment. The Company elected to take the optional exemption from applying IFRS 2 retrospectively for the |

c. |

Effect of transition to Taiwan-IFRSs |

| After transition to Taiwan-IFRSs, the effect on the Company’s consolidated balance sheets as of December 31, 2012 and January 1, 2012 (the transition date) as well as the consolidated statements of comprehensive income for the year ended December 31, 2012, is stated as follows: |

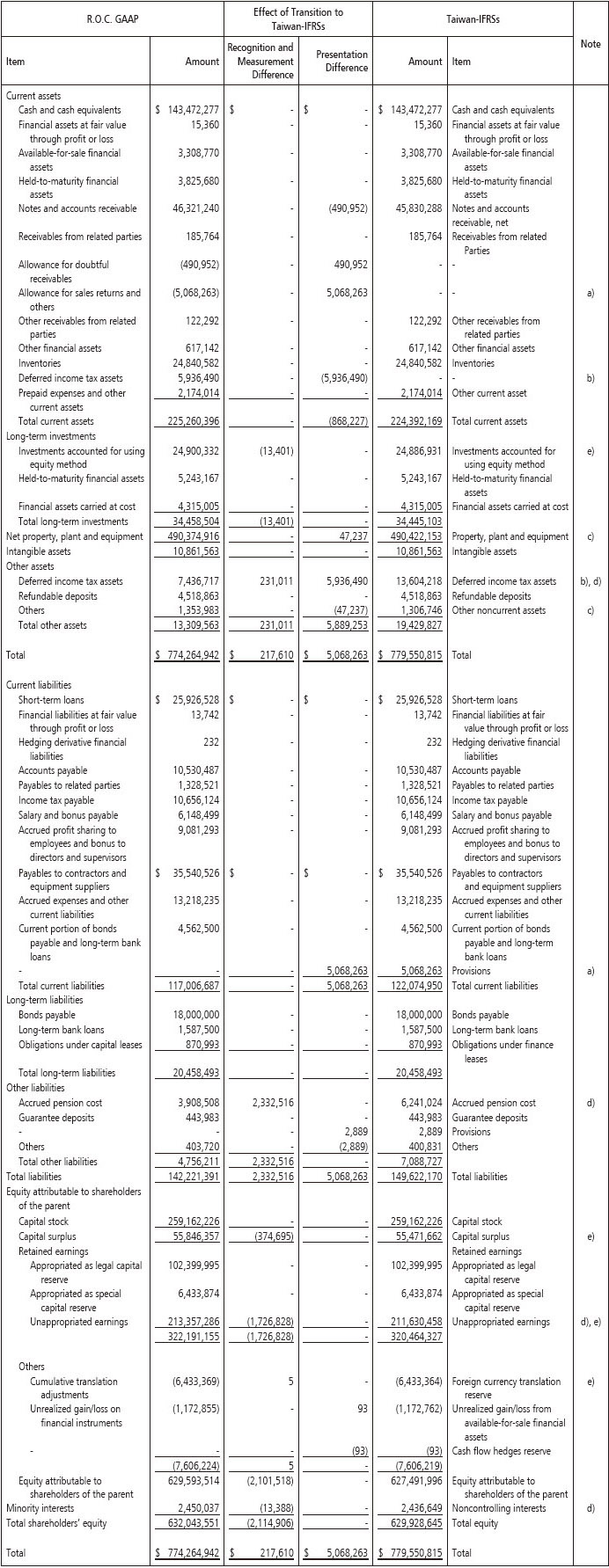

| 1) Reconciliation of consolidated balance sheet as of December 31, 2012 |

| 2) Reconciliation of consolidated balance sheet as of January 1, 2012 |

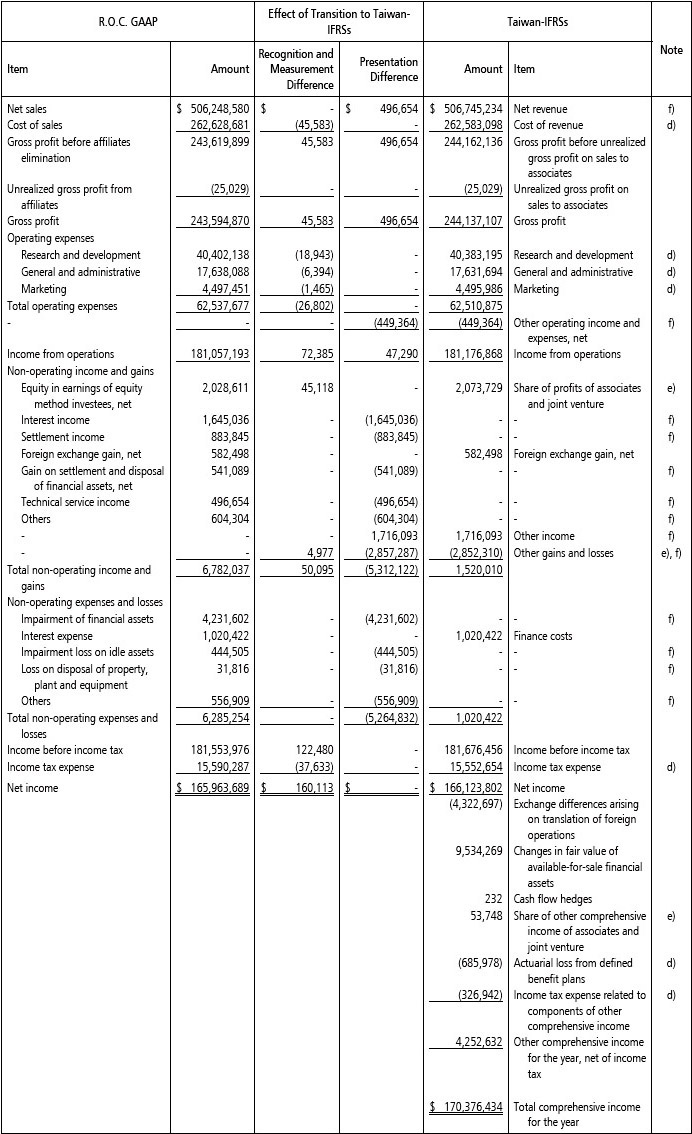

| 3) Reconciliation of consolidated statement of comprehensive income for the year ended December 31, 2012 |

| 4) Significant reconciliation differences in consolidated statements of cash flows for the year ended December 31, 2012 | |

The Company prepared the statement of cash flows using the indirect method under R.O.C. GAAP, in which the interest |

|

Except for the above differences, there are no other significant differences between R.O.C. GAAP and Taiwan-IFRSs in the |

d. |

Notes to the reconciliation of the significant differences: |

||||||||||||

|