and Independent Auditors’ Report

- REPRESENTATION LETTER

- INDEPENDENT AUDITORS' REPORT

- CONSOLIDATED BALANCE SHEETS

- CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

- CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

- CONSOLIDATED STATEMENTS OF CASH FLOWS

- NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

36. |

FINANCIAL INSTRUMENTS |

|---|

a. |

Categories of financial instruments |

b. |

Financial risk management objectives |

| The Company seeks to ensure sufficient cost-efficient funding readily available when needed. The Company manages its exposure to foreign currency risk, interest rate risk, equity price risk, credit risk and liquidity risk with the objective to reduce the potentially adverse effects the market uncertainties may have on its financial performance. The plans for material treasury activities are reviewed by Audit Committees and/or Board of Directors in accordance with procedures required by relevant regulations or internal controls. During the implementation of such plans, Corporate Treasury function must comply with certain treasury procedures that provide guiding principles for overall financial risk management and segregation of duties. |

c. |

Market risk |

| The Company is exposed to the market risks arising from changes in foreign exchange rates, interest rates and the prices in equity investments, and utilizes some derivative financial instruments to reduce the related risks. Foreign currency risk The Company also holds short-term borrowings in foreign currencies in proportion to its expected future cash flows. This allows foreign-currency-denominated borrowings to be serviced with expected future cash flows and provides a partial hedge against transaction translation exposure. The Company’s sensitivity analysis to foreign currency risk mainly focuses on the foreign currency monetary items at the end of the reporting period. Assuming an unfavorable 10% movement in the levels of foreign exchanges against the New Taiwan dollar, the net income for the years ended December 31, 2013 and 2012 would have decreased by NT$171,961 thousand and NT$719,882 thousand, respectively, after taking into consideration of the hedging contracts and the hedged items. Interest rate risk Assuming the amount of floating interest rate bank loans at the end of the reporting period had been outstanding for the entire period and all other variables were held constant, a hypothetical increase in interest rates of 100 basis point (1%) would have resulted in an increase in the interest expense, net of tax, by approximately NT$332 thousand and NT$12,346 thousand for the years ended December 31, 2013 and 2012, respectively. Other price risk Assuming a hypothetical decrease of 5% in equity prices of the equity investments at the end of the reporting period, the net income for the years ended December 31, 2013 and 2012 would have been unaffected as they were classified as available-for-sale; however, the other comprehensive income for the years ended December 31, 2013 and 2012 would have decreased by NT$931,881 thousand and NT$2,217,457 thousand, respectively. |

d. |

Credit risk management |

Credit risk refers to the risk that a counterparty will default on its contractual obligations resulting in financial loss to the Company. The Company is exposed to credit risk from operating activities, primarily trade receivables, and from financing activities, primarily deposits, fixed-income investments and other financial instruments with banks. Credit risk is managed separately for business related and financial related exposures. As of the end of the reporting period, the Company’s maximum credit risk exposure is mainly from the carrying amount of financial assets recognized in the consolidated balance sheet. Business related credit risk As of December 31, 2013 and 2012 and January 1, 2012, the Company’s ten largest customers accounted for 68%, 68% and 64% of accounts receivable, respectively. The Company believes the concentration of credit risk is insignificant for the remaining accounts receivable. Financial credit risk |

e. |

Liquidity risk management |

The objective of liquidity risk management is to ensure the Company has sufficient liquidity to fund its business requirements associated with existing operations over the next 12 months. The Company manages its liquidity risk by maintaining adequate cash and banking facilities. |

|

As of December 31, 2013 and 2012 and January 1, 2012, the unused of financing facilities of the Company amounted to NT$76,689,543 thousand, NT$53,422,331 thousand and NT$63,708,014 thousand, respectively. |

|

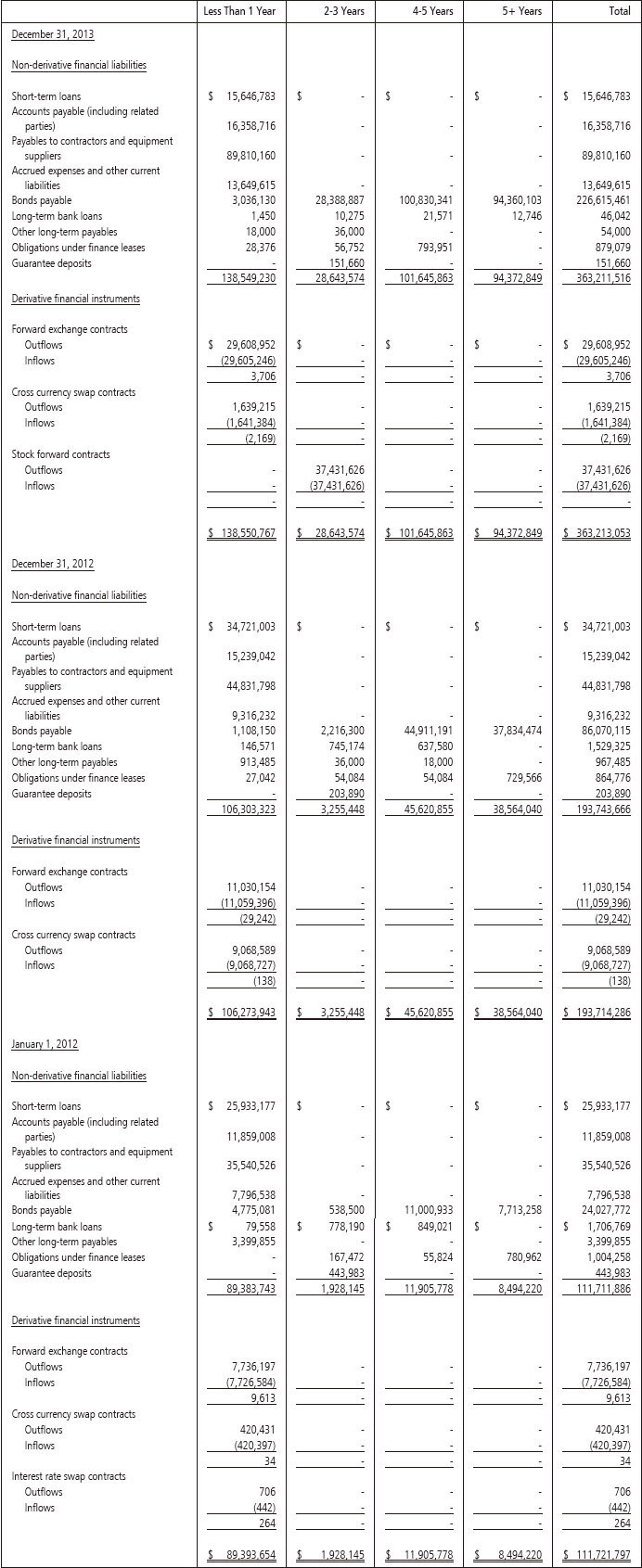

The table below summarizes the maturity profile of the Company’s financial liabilities based on contractual undiscounted payments, including principles and interests. |

f. |

Fair value of financial instruments |

| 1) Fair value of financial instruments carried at amortized cost

2) The following table provides an analysis of financial instruments that are measured subsequent to initial recognition at fair |

|

| There were no transfers between Level 1 and 2 for the years ended December 31, 2013 and 2012, respectively. There were no purchases and disposals for assets on Level 3 for the years ended December 31, 2013 and 2012, respectively. |

| 3) Valuation techniques and assumptions used in fair value measurement

|