and Independent Auditors’ Report

- REPRESENTATION LETTER

- INDEPENDENT AUDITORS' REPORT

- CONSOLIDATED BALANCE SHEETS

- CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

- CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

- CONSOLIDATED STATEMENTS OF CASH FLOWS

- NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

10. |

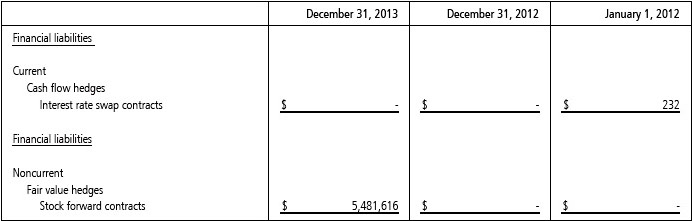

HEDGING DERIVATIVE FINANCIAL INSTRUMENTS |

|---|

The Company’s investments in publicly traded stocks are exposed to the risk of market price fluctuations. Accordingly, the Company entered into stock forward contracts to sell shares at a contracted price in a specific future period in order to hedge the fair value risk caused by changes in equity prices.

The outstanding stock forward contracts consisted of the following:

In addition, the Company’s long-term bank loans bear floating interest rates; therefore, changes in the market interest rate may cause future cash flows to be volatile. Accordingly, the Company entered into an interest rate swap contract in order to hedge cash flow risk caused by floating interest rates. The interest rate swap contract of the Company was due in August 2012. The contract information was as follows:

For the year ended December 31, 2012, the amount recognized in other comprehensive income and accumulated under the heading of cash flow hedges reserve from the above interest rate swap contract amounted to a net gain of NT$5 thousand; the amount reclassified from equity and recognized as a loss from the above interest rate swap contract amounted to a net loss of NT$227 thousand, which was included under finance costs in the consolidated statements of comprehensive income.